ICGI 04 -01 Empowering Auditors FEC Report for Audit Firms

ICGI 04 -01 Empowering Auditors

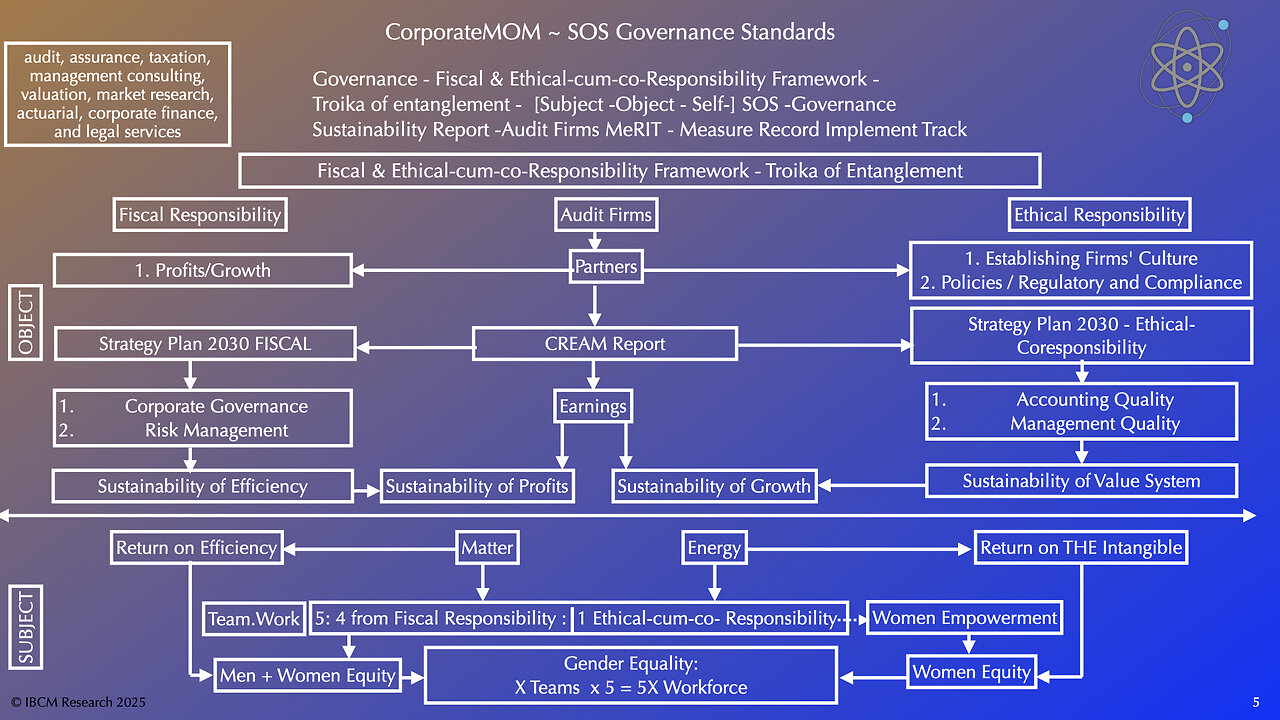

FEC Report for Audit Firms

Empowering Auditors

FEC Report for Audit Firms

1. ICAI must take steps to remove Intangible Assets and replace to a Standard ‘Capitalization of R&D and Development Costs’.

2. Then Audit Firms can feel good to restore GRACE. GOVERNANCE, RESPONSIBILITY, AUTHORITY, CREDIBILITY, ENABLEMENT

Balance Sheet is their territory and allowing a non-monetary so called asset to creep in, is their mistake entirely. Correct it now, now, now.

3. Let me present FEC and CREAM Report for Audit Firms enabling ICAI to prepare an SQM.

4. Entity analyzed as a Corporate Body .

Happy Pongal

PS: An extract from my book:

Quote:

It has a sting in the tail that was not deliberated threadbare during the exposure drafts discussions or at the review stage of IAS 38. The conditions are entirely different in capitalization between 1977 and 1995. There was no need to displace IAS 9 and substitute with IAS 38, enlarging the scope of assets covered. Such intangible assets could have remained or made use of, as off–balance sheet assets, without bringing them into the books of accounts. Even now, strictly an intellectual property right (IPR) is a work-in-progress and gets validated only if a patent is obtained. The balance sheet must be fortified to exclude non-transactional entries. The balance sheet is a simpleton, like a foolish or gullible person, ready to accept what one offers. One can’t keep adding frivolous ideas to it hoping that accounting standards would help remove inconsistencies. Inventory accounting also has several methods of valuation. Select one and keep it simple. Leave the balance sheet alone.UQ

-

LIVE

LIVE

I_Came_With_Fire_Podcast

9 hours agoCartels vs. America: Fentanyl's 2 Front Attack, and the Rise of CJNG

132 watching -

2:50:03

2:50:03

BlackDiamondGunsandGear

14 hours agoLIVE SHOW / CMMG/ DLD AFTER DARK

501 -

52:05

52:05

PMG

15 hours ago $0.01 earnedWhat Does Freedom Cost? Steven Solomon's On-the-Ground Documentary in Ukraine

429 -

9:45

9:45

RTT: Guns & Gear

16 hours ago1000 Rounds Of Awesome: Radical Defense Mk1 Mod 1 Patrol Rifle

174 -

7:42

7:42

Bek Lover Podcast

16 hours agoInteresting Times with Bek Lover Podcast

152 -

1:02:27

1:02:27

Weberz Way

14 hours agoICE IS IN FULL FORCE, TRUMP 2.0 IN L.A., & FUNDING IS CUT OFF

39 -

11:49

11:49

Ethical Preparedness

17 hours agoThe Post Collapse Emergency Food That You Don't Know About - Prepper Skills

2334 -

5:17

5:17

SeasonofMist

1 day agoVLTIMAS - Mephisto Manifesto (Official Music Video)

28 -

50:42

50:42

CutJibNewsletter

2 days agoThe Orange Mandela Delivers on Deliverance Episode!

22 -

25:30

25:30

SB Mowing

1 day agoFrom Overgrown to OVERJOYED - Busy Mom and her Kids can Enjoy the Yard Again

12.2K11