Duration and Convexity Calculations (Hull, Interest Rates)

2 months ago

7

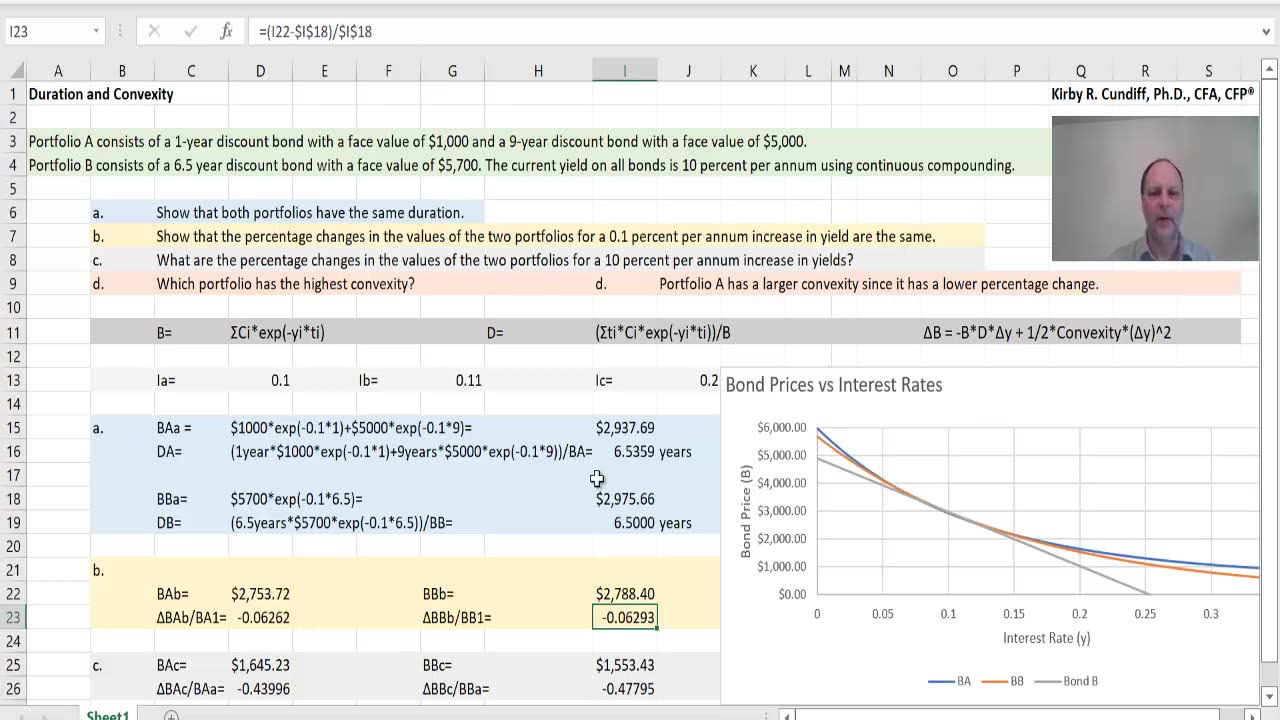

In this video I study duration and convexity calculations. How to calculate portfolio prices, and portfolio durations is discussed. How approximate changes in bond prices are calculated using a Taylor series involving duration and convexity terms is also discussed. The example we use is similar to a problem out of the Hull, "Options Futures, and Derivatives" text chapter on Interest Rates.

Loading 1 comment...

-

4:44:39

4:44:39

SoundBoardLord

8 hours ago90's Cartoons, Chill Vibes, Good Conversations - SATURDAY MORNINGS WITH CASEY

43.3K3 -

38:28

38:28

Anthony Pompliano

1 day ago $4.22 earnedPomp on BlackRock & Metaplanet Buying Bitcoin

62.9K -

36:01

36:01

TimcastIRL

18 hours agoThe Green Room #82 - Timcast Discord & Building Culture in the Digital Space with Roma Nation

84.8K13 -

1:00:59

1:00:59

IsaacButterfield

20 hours ago $2.14 earnedSHOCKING Nurses Rant About Killing Israelis | Kanye Bombshell | USAID Spending

28.8K23 -

11:38

11:38

MrBigKid

1 day ago $0.95 earnedSIG 556 Classic SWAT: The Swiss-Inspired Rifle for 'Merica

20.5K2 -

1:13:32

1:13:32

Tommy's Podcast

2 months agoMedia Decentralization | Sam Anthony (TPC #1,640)

16.2K1 -

1:01:05

1:01:05

Trumpet Daily

1 day ago $5.24 earnedMEGA Will Backfire on MAGA - Trumpet Daily | Feb. 14, 2025

15.2K20 -

1:42:23

1:42:23

Game On!

17 hours ago $4.63 earnedEagles Super Bowl Parade EPIC Fail!

36K9 -

3:29:22

3:29:22

FreshandFit

17 hours agoFresh&Fit After Hours Valentine's Day Edition

192K159 -

35:31

35:31

SB Mowing

1 day agoThis FORGOTTEN property needed a MIRACLE after nearly a DECADE of ruin

195K53